How To Invest Hsa Money

[Updated in November 2018 after Fidelity Investments started offering HSA to the general public.]

An Health Savings Account (HSA) has triple tax benefits: tax deductible contributions going into the account, tax free growth within the account, and tax free distributions coming out the account if used for eligible medical expenses. In addition, the required High Deductible Health Plan (HDHP) usually has a lower premium. For most people who are healthy, HDHP + HSA is the best combination. See Do The Math: HMO/PPO vs High Deductible Plan With HSA.

The money contributed to the HSA can be invested for long-term growth. However, until recently, it wasn't easy to find a no-fee HSA provider with good investment options. Most HSA providers usually require any combination of:

- A monthly or annual maintenance fee

- A minimum amount that must be held in cash

- Transfers between one entity holding cash and another entity holding investments

- A limited investment menu, sometimes with additional expenses on top of normal fund expenses

Now an industry giant entered the room. Fidelity Investments started offering HSA to the general public on November 15, 2018. Fidelity used to offer HSA only to people whose employer chose Fidelity as the HSA provider. Now individuals can open HSA on their own directly with Fidelity. When you have an HSA directly with Fidelity, not through an employer or an insurance company, you will have:

- No minimum amount to open the account

- No monthly or annual maintenance fee

- No minimum balance that must be held in cash

- Just one integrated account; no transfers back and forth between different entities

- All the investment options available in a regular Fidelity brokerage account, including commission-free low-cost index funds, ETFs, Treasuries, CDs, and more. See also: Best Index Funds and ETFs at Fidelity.

No other HSA provider comes close to what Fidelity offers. Compare with some other popular HSA providers that offer investments:

Lively: transfer between Lively and TD Ameritrade for investments.

HSA Bank: monthly fee if not holding a minimum amount in cash; transfer between HSA Bank and TD Ameritrade for investments.

HSA Authority: annual fee; fixed menu of investments.

Further: monthly fee; fixed menu of investments or transfer between Further and Charles Schwab.

Saturna Brokerage: higher-expense mutual funds or commission on each investment purchase and sale.

Bank of America: monthly fee (waived for highest tier in Preferred Rewards); fixed menu of investments.

Through Your Employer AND On Your Own

If you have a High Deductible Health Plan (HDHP) through your employer, your employer may already set up a linked HSA for you at a chosen provider. Your employer may be contributing an amount on your behalf there. Your payroll contributions also go into that account. Your employer may be paying the fees for you on that HSA. You save Social Security and Medicare taxes when you contribute to the HSA through payroll.

That doesn't stop you from having another HSA on your own. You can have two HSAs at the same time. The investment options in the HSA chosen by your employer may not be as good as those in a Fidelity HSA. After the contributions are made to the HSA chosen by your employer, you can move the money to your own HSA for better investment options. You can keep the existing HSA open to accept additional contributions. When you leave the employer or when you no longer have an HDHP, you can close the existing HSA and consolidate into your own HSA.

If you get health insurance outside an employer, you are on your own. The insurance company may offer an HSA but you are free to choose your own provider. You get the tax deduction on your tax return.

Transfer From an Existing HSA

If you'd like to move money an existing HSA to a new HSA, you can do it either as a transfer or as a rollover.

A transfer doesn't pass through you. There is no frequency limit on transfers. You don't receive any 1099 forms for transfers. You don't have to report transfers on your tax return. However, your HSA provider may charge you a fee for the outgoing transfer (some banks and credit unions don't charge).

You start the transfer by filling out a transfer request from the new HSA provider. A transfer can be full or partial. You send the completed transfer request with any required documents to the new HSA provider. They will take it from there and request the transfer from your current HSA provider. Your current provider may charge you a fee for the outgoing transfer or account closure. If the account will still receive payroll contributions, you can tell the current HSA provider to keep the existing account open when you do the transfer.

To request a transfer into your Fidelity HSA, you can do it online:

![]()

Click on Transfer and then See more transfer options.

![]()

Click on Transfer Assets from Anther Financial Institution in the next screen and follow the steps from there. You will be asked for a recent account statement from your other HSA.

Some HSA providers can transfer investments out without selling them. Some HSA providers can only transfer out cash, in which case you will have to sell the investments in your existing HSA to cash first before you request the transfer. Selling investments inside the HSA is not taxable at the federal level. It's not taxable in most states either, except in California and New Jersey, where selling investments inside an HSA is treated as a taxable event at state income tax level.

Rollover

If your existing HSA provider charges a fee for the outgoing transfer and you'd like to avoid the fee, you can do a rollover yourself, but you can only do it once per rolling one-year period (not calendar year). A rollover can only be done in cash. You request a distribution from your current HSA provider as you normally would when you reimburse yourself for eligible medical expenses. The distribution is deposited into a personal checking account. Then you send a check within 60 days to the new HSA provider as a rollover contribution.

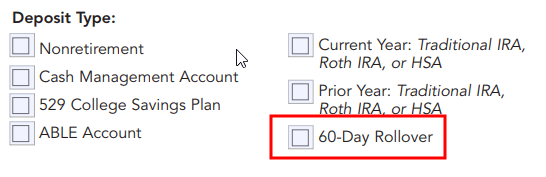

Rollover and normal contributions are reported differently by the receiving HSA provider to the IRS. While there's an annual dollar limit for normal contributions, there is no dollar limit for a rollover. When you send the rollover to your new HSA provider, be sure to indicate the money is a rollover, not a normal contribution. That way it doesn't use up the annual limit for your normal contributions. For rolling over into a Fidelity HSA, attach your check to a completed Deposit Slip and mark the box for "60-Day Rollover."

After the end of the year, the HSA provider that distributed the money will send you a Form 1099-SA showing the distribution. You will report on IRS Form 8889 line 14b how much of the distribution was rolled over. The amount rolled over isn't taxable. In May each year, the receiving HSA provider will send you a Form 5498-SA, which confirms the normal contributions and the rollover received in the previous year. Save the 1099-SA and the 5498-SA in your tax files to show that you did a rollover if you are ever asked for proof.

See also: How To Rollover an HSA On Your Own and Avoid Trustee Transfer Fee

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Find Advice-Only

How To Invest Hsa Money

Source: https://thefinancebuff.com/best-hsa-provider-for-investing-hsa-money.html

Posted by: matoslauted.blogspot.com

0 Response to "How To Invest Hsa Money"

Post a Comment